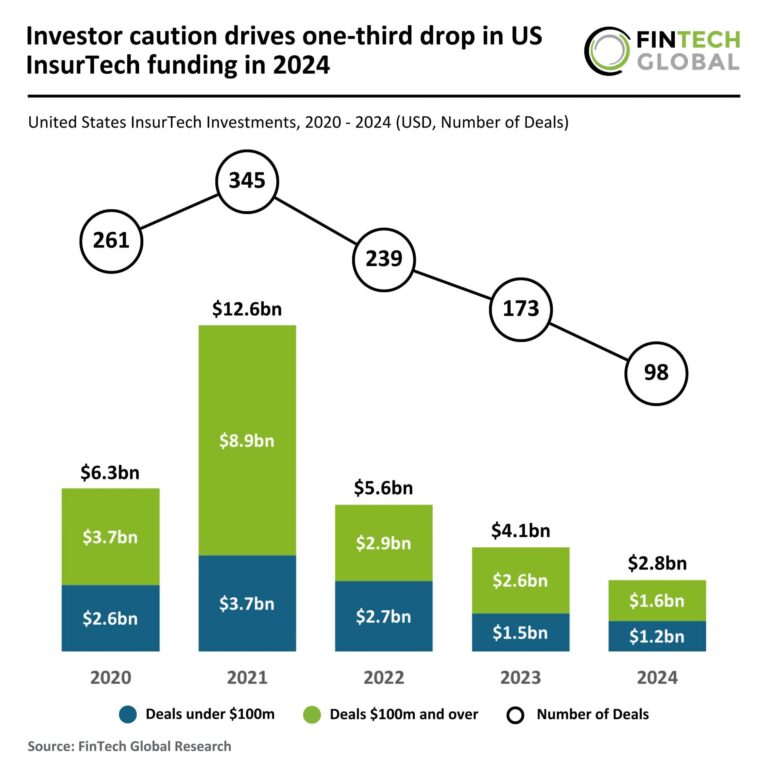

UK Dominates European InsurTech Landscape in 2024, Capturing One-Third of All Investment Deals

In 2024, the European InsurTech investment landscape faced significant challenges, with a notable drop in deal activity and funding. This article explores the key statistics and trends shaping the InsurTech sector across Europe, highlighting the performance of leading countries and major players in the industry.

Decline in European InsurTech Deal Activity

The European InsurTech sector experienced a substantial downturn in 2024, as both funding and deal activity saw a decline compared to previous years. Specifically:

- Total funding decreased to $1.7 billion, which is a 25% drop from $2.2 billion in 2023 and a staggering 62% decline from $4.4 billion in 2020.

- Deal volume also fell sharply, with only 75 deals completed in 2024, marking a 54% decrease from 164 deals in 2023 and a 73% drop from 273 deals in 2020.

This decline illustrates the ongoing challenges faced by the InsurTech sector, influenced by a cautious investment climate and evolving market dynamics that have affected deal flow.

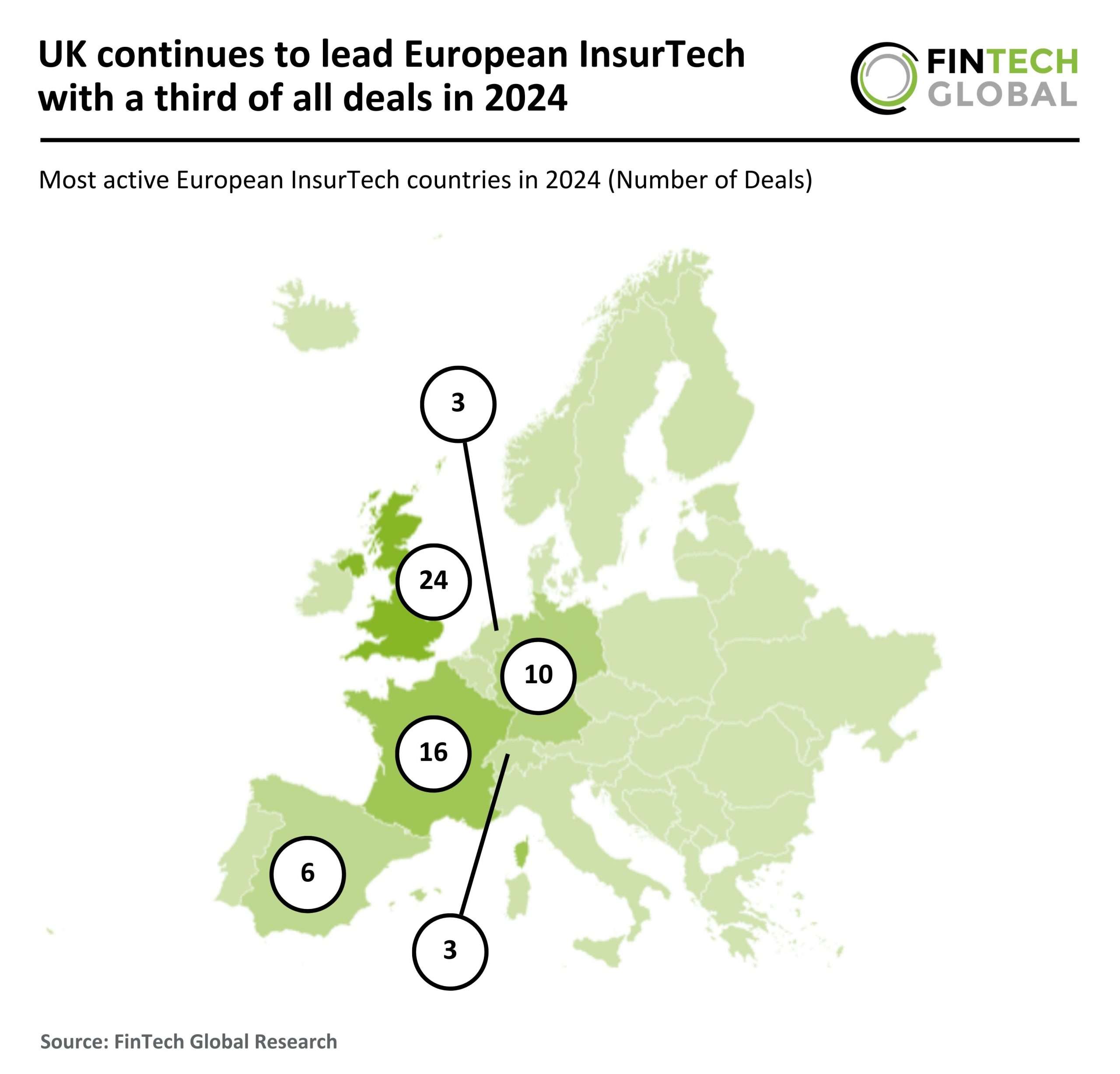

The UK Remains a Leading InsurTech Hub

Despite the overall downturn, the United Kingdom solidified its position as the top European InsurTech hub in 2024. Key highlights include:

- The UK completed 24 deals, accounting for a 32% share of the total market, although this represents a 54% decline from 52 deals in 2023.

- France maintained its second-place ranking with 16 deals (21% share), down from 27 deals in the prior year.

- Germany followed with 10 deals (13% share), reflecting a 44% decrease from 18 deals in 2023.

The UK’s continued dominance in the InsurTech space, alongside France’s increased market share, highlights the shifting dynamics within the European InsurTech landscape.

Major Players in the InsurTech Sector

One of the standout performers in 2024 was hyperexponential, a leader in pricing decision intelligence (PDI) software. The company secured one of the largest InsurTech deals of the year with a Series B funding round of $73 million.

hyperexponential’s innovative PDI platform, hx Renew, enables insurers to:

- Utilize large and alternative datasets.

- Rapidly develop and refine rating tools.

- Employ advanced machine learning techniques for risk pricing and data-driven decision-making.

Since its Series A funding in 2021, hyperexponential has achieved a remarkable 10x growth in sales while maintaining profitability, serving globally recognized insurers such as Aviva, HDI, and Conduit Re.

Future Outlook for the European InsurTech Market

Looking forward, hyperexponential plans to expand its reach into the United States, with plans to establish a New York office. This expansion will enable enhanced investment in new product capabilities to meet rising client demand, particularly in the small and medium-sized enterprise (SME) insurance sector.

The company aims to double its workforce, targeting over 200 employees by 2025, as it seeks to navigate the evolving InsurTech landscape amid ongoing challenges.

For more insights on the InsurTech industry, visit our InsurTech Insights page.